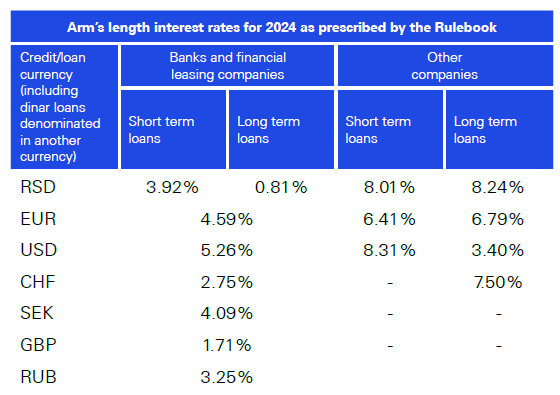

Serbia: Rulebook on arm’s length interest rates for 2025

Personal Loans in Serbia

Personal loans in Serbia are unsecured credit options designed for various individual needs, such as education, medical expenses, or travel. These loans do not require collateral, making them accessible but often carrying higher interest rates to offset the risk for lenders. Banks like UniCredit and Raiffeisen offer personal loans with amounts up to 3,000,000 RSD and repayment periods from 12 to 84 months. Interest rates are typically fixed, ranging from 7% to 12%, with effective annual rates (EIR) including fees pushing this to 8-14%. To apply, applicants need a stable income source, usually verified through payroll statements or tax returns, and a positive credit report from the Credit Bureau of Serbia. Non-residents may face stricter requirements, including residency permits. Processing times average 1-3 days for approvals, with funds disbursed directly to bank accounts. Borrowers should note that early repayment might incur penalties, and defaulting can lead to legal actions affecting future creditworthiness. In comparison to other consumer credits, personal loans provide flexibility without asset pledging, but careful budgeting is essential to manage monthly installments. Data from the National Bank indicates that personal loan uptake has increased by about 5% annually, driven by rising living costs.

![]()

2+ Thousand Micro Loan Royalty-Free Images, Stock Photos …

Business Loans in Serbia

Business loans support entrepreneurial activities and company expansions in Serbia, catering to small and medium enterprises (SMEs) which form a significant part of the economy. These loans can be short-term for working capital or long-term for investments in equipment or real estate. Institutions like ProCredit Bank and OTP Bank provide options with amounts starting from 500,000 RSD up to several million euros, depending on the business’s financial health. Interest rates vary: fixed rates around 5-8% for dinar loans, or variable rates linked to 6M EURIBOR plus a margin of 2-4%. Requirements include business registration documents, financial statements for the past two years, and sometimes collateral like property or inventory. The government-backed Guarantee Fund offers partial guarantees to reduce risk, encouraging lending to startups. Approval processes involve credit assessments and may take 1-4 weeks. Repayment terms extend up to 10 years, with grace periods for initial months. Economic reports show that business lending grew by 7% in 2024, amid efforts to boost private sector growth. However, high inflation can increase borrowing costs, and businesses must demonstrate viable cash flows to qualify. This type of financing plays a role in Serbia’s transition to a market-oriented economy.

Bridging Entrepreneurial Intention and Action: How Financing …

Home Loans in Serbia and Comparisons with Germany

Home loans in Serbia facilitate property purchases or renovations, often structured as mortgages with real estate as collateral. Banks such as Banca Intesa and Postal Savings Bank offer these with minimum down payments of 10-20%, though 20% is more common to secure better terms. Loan amounts can reach up to 80% of the property value, with terms up to 30 years. Interest rates include fixed options at 3.8-5% or variable ones based on 3M EURIBOR plus 1.86-3%. For non-residents, rates are variable and adjusted periodically. The effective interest rate (EIR) factors in processing fees, insurance, and notary costs, typically adding 0.5-1% to the nominal rate. Applicants need income proof, property appraisals, and life insurance policies. In contrast to Germany, where mortgage rates average 3.74% and the price-to-income ratio is lower (around 10.23 in Berlin versus 16.47 in Belgrade), Serbia’s higher rates (5.31% real) reflect greater economic volatility. German loans benefit from stable EU regulations, with mortgage burdens at 72% of income compared to Serbia’s 135%. However, Serbia’s lower overall living costs (59% less than Germany) make home ownership more attainable for locals, despite higher relative debt loads. Cross-border borrowers might find Serbian options appealing for investment properties.

Mandarina Reserve – A New Home Community by KB Home

Mortgage Loan Calculators in Serbia

Mortgage loan calculators are tools used by potential borrowers in Serbia to estimate monthly payments, total interest, and affordability before applying. Available on bank websites like OTP Bank or independent platforms, these calculators input variables such as loan amount, interest rate, term, and down payment. For example, a 100,000 EUR mortgage at 4% fixed rate over 25 years might yield monthly payments of about 527 EUR, with total interest exceeding 58,000 EUR. Variable rate scenarios incorporate EURIBOR fluctuations, showing potential increases if rates rise. Users can adjust for fees, like 1% processing costs, to get a realistic EIR. These tools help compare offers across banks, factoring in currency (euro vs. dinar) and repayment schedules. In Serbia, where housing prices in Belgrade average 2,500-3,500 EUR per square meter, calculators reveal that a 20% down payment reduces risk and rates. They also simulate amortization tables, illustrating how principal and interest portions change over time. According to market data, using calculators can prevent overborrowing, as Serbia’s high price-to-income ratio demands careful planning. Similar tools exist for refinancing, allowing users to input current loan details for potential savings.

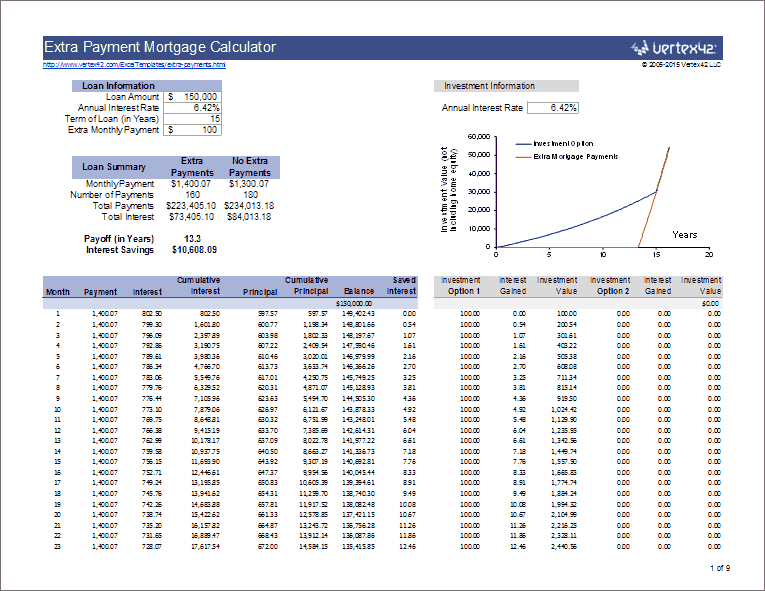

Extra Payment Mortgage Calculator for Excel

Car Loan Calculators in Serbia

Car loan calculators assist Serbian consumers in planning vehicle purchases by computing financing costs. Offered by banks like Adriatic Bank, these online tools require inputs like vehicle price, down payment (often 20-30%), interest rate (typically 5-9%), and loan duration (up to 7 years). For a 20,000 EUR car with 10% down and 6% rate over 5 years, monthly installments might be around 348 EUR, with total interest of about 2,880 EUR. Calculators account for variable rates if tied to benchmarks and include fees such as insurance or registration. They provide breakdowns of principal repayment and help compare new versus used car financing, where used vehicles may have higher rates due to risk. In Serbia, where car ownership is common but import duties affect prices, these tools highlight affordability amid average salaries of 700-900 EUR monthly. Users can test scenarios for early payoffs, reducing interest. Data from the Association of Serbian Banks shows car loans comprise 15% of consumer credit, with calculators promoting informed decisions to avoid defaults.

Auto Loan Calculator % – You Might Also Like – App Store

Cash Credit Loans in Serbia

Cash credit loans in Serbia provide immediate liquidity for short-term needs, functioning as overdrafts or revolving credit lines. Banks like Yettel Bank offer these with limits up to 3,500,000 RSD and fixed rates around 8.6%. Unlike traditional loans, interest accrues only on the used amount, with flexible drawdowns and repayments. Requirements include a current account with the bank, income verification, and credit checks. Terms allow for renewal upon review, but overuse can lead to higher costs due to daily interest calculations. These loans suit emergencies or bridging income gaps, with approval in hours for existing clients. In Serbia’s economy, where inflation averages 4-6%, cash credit helps manage cash flow without long-term commitments. However, EIR can reach 10-12% with fees, so monitoring usage is key. Reports indicate that such products have seen 10% growth in uptake, reflecting consumer demand for quick access to funds.

Bank Credit, Loan Payment Flat Vector Illustration Stock Vector …

Conclusion: Navigating Loans in Serbia

In summary, Serbia’s loan market provides diverse options tailored to personal, business, and asset-based needs, with rates and terms shaped by economic indicators and banking regulations. Borrowers benefit from tools like calculators for informed choices, while comparisons with countries like Germany highlight differences in costs and accessibility. Understanding requirements and risks is essential for sustainable borrowing in this context.

Conclusion: the impact of the ‘debt system’